A couple of weeks after the release of the Housing Price Index for the first quarter of 2017, we updated the median home price per county[1]. Applying the price change in the related metropolitan areas to every county, it seems that, compared to a year earlier, home prices continue to rise in 98 percent of counties. Counties in the following metro areas experienced price gains higher than 12 percent:

Sebring, FL

Bremerton-Silverdale, WA

Grants Pass, OR

Palm Bay-Melbourne-Titusville, FL

Longview, WA

Homosassa Springs, FL

Sebastian-Vero Beach, FL

Punta Gorda, FL

Seattle-Bellevue-Everett, WA

Meanwhile mortgage rates fall back. After a four-month spike following the elections, mortgage rates have started to move the other direction. Based on Freddie Mac, the average rate for a 30-year fixed mortgage was 4.2 percent in March while it decreased to 4.05 percent in April and it dropped further to 4.01 percent in May. Mortgage rates are still historically low, but crossing over from the 3 percent range to 4 percent range might concern some potential homebuyers.

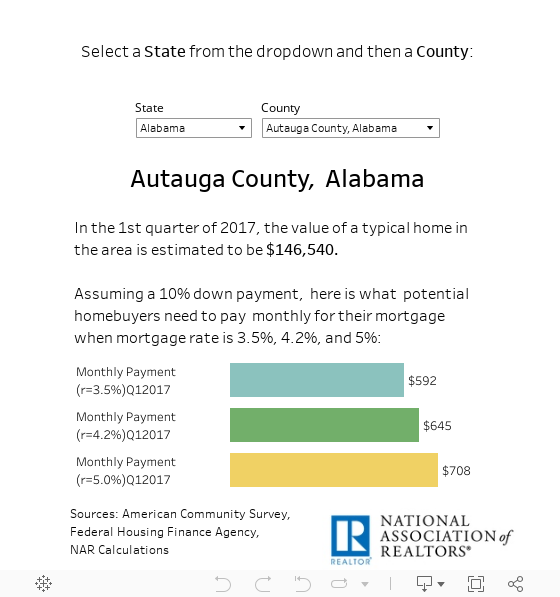

We calculated the monthly payment by county based on the mortgage rate in October (3.5 percent), the rate as of March (4.2 percent) and a higher rate likely to be seen within the next two years (5.0 percent).

Nationwide, it is estimated that the rise of mortgage rates from 3.5 to 4.2 percent increased the monthly payment by $76 to the amount of $928 while a rise from 4.2 to 5.0 percent will increase the monthly payments by $91[2] (to $1,019 per month).

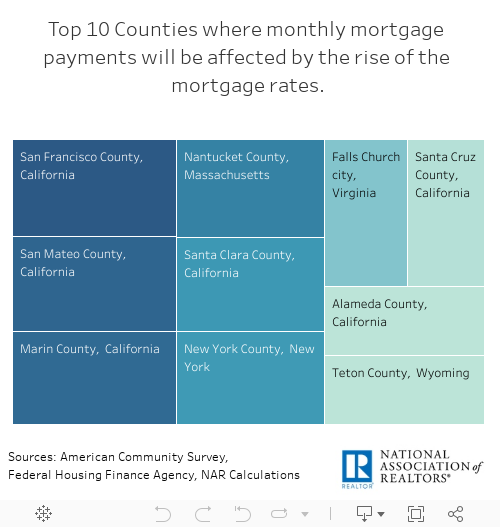

But the effect depends on the location. At the high end, San Francisco homebuyers have seen a nearly $384 increase in monthly payments so far, and if rates were even higher now, financing the same-priced home would cost an extra $459 per month. At the low end, in Cochran County, TX, home buyers are paying an extra $13 per month on account of the mortgage rate rise since November, and they could see an extra $16 per month as rates rise to 5 percent. At this end of the spectrum, the change in monthly payments seems much more manageable.

However, these examples only use the current price of homes to see the difference. In the years ahead, NAR expects that the 30 year fixed-rate will increase to 4.3 percent in 2017 and 5.0 percent in 2018 while home prices are expected to rise 5.0 and 3.5 percent, accordingly. Rising prices in addition to rising mortgage rates will push the monthly cost of housing up even higher for new homebuyers. Existing homeowners who took out fixed rate mortgages will have the same monthly principal and interest payment.

Select a County from the dropdown and see how much monthly payments change over the different mortgage rates:

Lastly, please take look at which counties will be affect mostly from the increase of mortgages rates:

[1] There is data available for 3,119 counties. For counties in Metropolitan Statistical Areas (MSAs), the growth rate is assumed to be the same as the MSA. For counties outside of MSAs, a non-MSA growth rate for each state is applied.

[2] The U.S. median home value matches the county prices calculations. For comparisons purposes, the calculated median home value reflects all homes while NAR’s U.S. median price represents home sales. Thus, the calculated price ($210,817) is expected to be lower than NAR’s home value ($230,700 in Q1 2017). Please see Methodology for more details. Also note that the impact of rate changes by in each MSA is estimated on current quarter prices.