Just over a year ago, China overtook the U.S. as the world’s largest economy. Since then, China’s importance on the global economic stage has only expanded. Some of the most significant developments, outlined here, could impact China’s enthusiasm for global real estate.

Unleashing the Yuan

Cautiously, but deliberately, Beijing has been taking signifi cant steps aimed at deregulating China’s capital markets and turning the renminbi into a global currency. Among the most important liberalization efforts:

Qualified Domestic Individual Investor program:

Commonly called QDII2 (a second iteration of an earlier program limited to institutions), the new rules will allow Chinese individuals direct access to overseas investments at much higher levels than the current offi cial cap of US$50,000.

Once launched, the pilot program will include six Chinese cities (Shanghai, Tianjin, Chongqing, Wuhan, Shenzhen and Wenzhou) and will be open to individuals with fi nancial assets of at least 1 million yuan (US$160,000), potentially unleashing billions of dollars in Chinese savings on global stock and bond markets. Eligible investment classes are expected to include:

- Equity shares, bonds, funds, insurance products, foreign exchange and derivative products

- Greenfield and joint venture projects

- Real estate

Once satisfied the program is not generating excessive capital flight or volatility, QDII2 could be expanded more broadly.

Foreign-owned investment management firms:

Traditionally, off shore fund managers had to partner with local managers via joint venture arrangements with 49 percent off shore ownership caps. Off shore fund managers are now being given direct access to Chinese HNW investors and are allowed 100 percent foreign ownership of private managed funds operating in China.

No interest rate ceiling on bank deposits:

In October, 2015, the People’s Bank of China (China’s central bank), took a major step towards financial reform by lifting its long-held interest rate restrictions. This allows banks’ rates to refl ect market conditions and compete more directly with the shadow banking sector’s wealth management products.

Devaluation:

Last August, the People’s Bank of China rocked the global markets with back-to-back devaluations of the renminbi. Its move triggered a major selloff in the stock market and left Chinese investors nervous about further erosion in their overseas buying power. Many have opted to move money off shore sooner rather than later, putting additional downward pressure on the renminbi.

IMF Weighs In

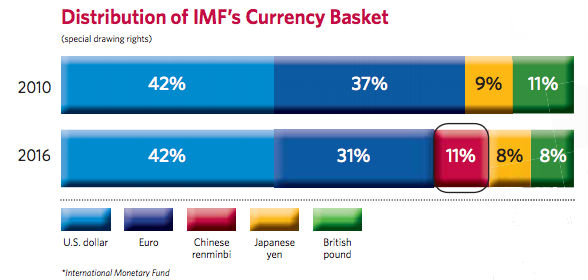

Late in November, China achieved its long-term goal of inclusion in the International Monetary Fund’s (IMF) official basket of currencies, frequently used as a benchmark in many central banks’ reserve measurements. The decision, effective late-September 2016, is largely symbolic, but does give the renminbi new global status, placing it in the company of the dollar, the euro, the pound and the yen. (See chart.)

In all likelihood, Beijing will need to take additional steps to deepen its financial system and make its economy more transparent before central banks fully embrace the renminbi as a reserve currency. In spite of efforts to loosen its grip, China still maintains heavy regulatory control over its financial system and faces strong internal opposition to further reforms, which could grow more acute if China’s economy continues to soften.

Emergence of a New Global Bank

For the past two years, China has championed the creation of a new multinational, multibillion-dollar bank to rival organizations like the World Bank, the International Monetary Fund (IMF) and the Asian Development Bank. Named the Asian Infrastructure Investment Bank, its stated purpose is to finance roads, rails, power grids and similar projects across Asia to spur economic development, especially in poor areas, and to promote the region’s position as a world wealth center.

In spite of concerns that China’s true objective is to promote its own global status and economic agenda—while forgoing key Western priorities like environmental and human rights protections—57 nations have signed up, as of this writing, rationalizing that China can’t be ignored and it’s better to work within the framework of the new bank.

What’s in a Name?

China’s currency, which goes by many names, is a frequent point of confusion. If you’re working with Chinese clients, you’ll want to understand the diff erent terms:

Yuan - The Chinese word for “dollar,” historically a silver coin used for centuries of global trade. It is also called Chinese Yuan and abbreviated CNY.

Renminbi (RMB) - Translated as “the people’s currency,” this is the offi cial name of China’s currency, introduced by the Communist Party in 1949. Use this term when referring to the currency markets, but not as a unit of money. (It isn’t correct, for example, to say something costs 10 renminbi.)

Kuai - Chinese nationals are most likely to use this term (instead of yuan or renminbi) which means “piece” (similar to a coin). Kuai is a colloquial word for money, much like “buck” in the U.S.

Mao, Jiao and Fen - These are also colloquial terms, referring to smaller units. Mao and jiao are used interchangeably, although mao is more common (and has no connection to Mao Zedong). One yuan equals 10 mao (or jiao), and one mao (or jiao) equals 10 fen.

The U.S. and Japan remain on the sidelines, while many key allies, including Britain, Germany, Australia and South Korea have joined. At $100 billion, the bank’s total capital commitment is already double the amount originally envisioned. Initial projects are expected to be selected shortly.

Latest Development Plan

Every five years, China’s leaders issue a new development plan—a significant document that establishes key goals for the country’s future social development and economic growth. The 13th Five-Year Plan, the first such plan under President Xi Jinping’s leadership, will run from 2016 to 2020. While the latest plan won’t be fi nalized until March, key elements are expected to include:

Economic growth—China has struggled to meet its previous GDP targets and appears to be aiming for a more modest 6.5 percent annual growth rate.

Green development—A stronger audit system will aim to improve environmental protections. Future economic growth will be achieved in tandem with a stabilization of energy consumption and greenhouse gas emissions.

Innovation—Technological upgrades in both the industrial and services industries will increase productivity, profitability, and promote higher wages from skill-intensive jobs.

Financial reforms—Further easing of restrictions and promoting market transparency are top priorities, reflected by steps already taken in this direction.

Other goals encompass health care, education, societal gains, agriculture, the military, and more. Many critics argue, however, that China’s ultimate challenge involves pitting its GDP goals against other objectives. Still, anyone interested in understanding China’s future should read the final 13th Five-Year Plan when it’s released, as it provides as much insight as one can get into the priorities of China’s leadership.

What Happens Next?

Analysts view China’s long-term economic picture as murky, with bearish opinions generally outnumbering the bulls. Doubts are further fueled by broad speculation that China is overstating its economic growth (officially 6.9 percent for Q3 2015) by at least two percentage points. China’s economy may be facing headwinds, but fi nancial reforms are likely to proceed, generally viewed as necessary for its long-term growth. In the near-term, analysts will continue to closely monitor the Chinese economy to see if sub-par economic growth translates into additional currency devaluations and fi nancial market volatility at home and abroad.