First-time buyers accounted for 32 percent of all buyers of existing homes in December 2017, also the full-year average, according to the December 2017 REALTORS® Confidence Index Survey.[1] Compared to 2016, the share held steady, even as home prices continued to increase at a much faster pace than income and as mortgage rates rose somewhat.

The share of first-time buyers started to pick up in 2016, but plateaued amid rising home prices. The median price of existing homes rose to $246,800 in December 2017, up six percent from the same month one year ago, while average weekly earnings were up by only three percent. Since January 2012, the median price of existing homes sold has increased by 61 percent, compared to the 20 percent growth in median household income. Meanwhile, the 30-year fixed rate averaged 3.99 percent in 2017, slightly up from 3.65 percent in 2016, following the cumulative one percentage point increase in the federal funds rate target rate since December 2016.[2]

Debt to Income Ratios Near 30 Percent for 25-34 Age Group

Amid rising home prices, first-time buyers are likely finding it hard to make a home purchase. Among households where the head of household is in the 25-34 years old age group, I calculated the share of owner costs (principal, interest, taxes, mortgage insurance, and home maintenance) at various down payment levels. Table 1 below shows that at the median income of $62,760, potential buyers who intend to put down 3.5%, 5%, or 10% down payment will be cost-burdened, spending nearly 30 percent of household income on housing expenses (principal, interest, property tax, insurance, and maintenance). If they make a 20 percent down payment, the share of housing expenses falls to 23 percent of income, but making the required down payment (nearly $40,000) may be a hurdle, given that the average savings of non-homeowners was only $5,200 in 2016, according to the Federal Reserve Board’s 2016 Survey of Consumer Finances.[3] As the same table shows, 25-34 year old households need to be making about $70,801 to $76,394 to keep household expenses at 25 percent of income, if they make a down payment of 3.5%, 5%, or 10%.

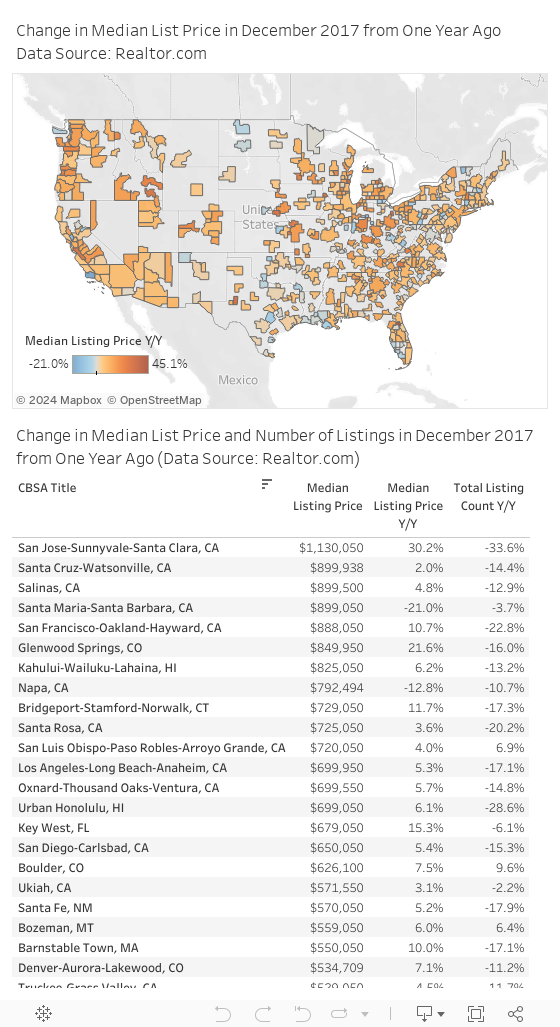

76 Percent of Metro Areas Had Fewer Listings, and 86 Percent Had Higher Median List Price

Across metro areas covering both high-price and low-price markets, home prices are rising due to tight inventory and strong demand, according to data from Realtor.com.

Of the 500 metro areas being tracked by Realtor.com, 380 metro areas, or 76 percent, had fewer listings in December 2017 compared to one year ago, and 430 metro areas, or 86 percent, had list prices that were higher than one year ago. Prices continue to increase even in already high-price areas. For example, San Jose-Sta. Clara-Sunnyvale, the median list price in December 2017 was $1.13 million, up by 30 percent from one year ago, with 33 percent fewer listings compared to one year ago.

In Seattle-Tacoma-Bellevue, the median list price was $495,0045, up by 16 percent, even as the number of homes listed rose 64 percent compared to one year ago, with prices rising likely on account of strong demand.

Meanwhile, supply is easing the price pressure in some metro areas. In Austin-Round Rock, TX, the median list price was $360,050, down by 6.5 percent, as the number of listings rose 9.5 percent from one year ago.

Recent fires in California in November also had some price effect. In Santa Maria-Santa Barbara, the median home price was $899,060, down by 21 percent. The number of listings slightly declined by nearly four percent.

See the interactive data visualization below to check out the data across metro areas.

[1]NAR’s 2017 Home Buyers and Sellers Report (HBS) reported the share of first-time buyers at 34 percent. The HBS report is survey of homebuyers who purchased the home for primary residence, while the NAR RCI Survey is a survey of REALTORS® who reported sales for primary and non-primary residential use of the buyer.

[3] Relaxed gifting standards within reasonable underwriting guidelines can also make a home purchase more affordable. For example, Fannie Mae allows all the down payment for one-unit principal residence property mortgages with loan-to-value of greater than 80 percent (or down payment of 19 percent or less) to come from eligible givers (persons related by blood or marriage, fiancé, fiancée, or domestic partner.[3] Freddie Mac allows gifts/grants after the borrower puts in a three percent down payment.[3] The Federal Housing Administration allows the 3.5 percent down payment to come from acceptable donors (relatives, employer, friend, charitable organization, government agency) for borrowers with credit score of at least 620. However, if credit score is between 580 and 619, the down payment must be the borrower’s own money (required minimum investment). The builder, seller, or an associated entity to the transaction may not provide gifts.