Mortgage rates dropped below 2.8% following the trend of the 10-year Treasury yield. Investors seem to be worried about the potential economic impact of the Delta variant drawing down both the 10-year Treasury yield and mortgage rates. Specifically, according to the mortgage finance provider Freddie Mac, the 30-year fixed mortgage rate fell to 2.77% from 2.80% the previous week. This translates to more homebuyers that will be able to benefit from the historically low mortgage rates.

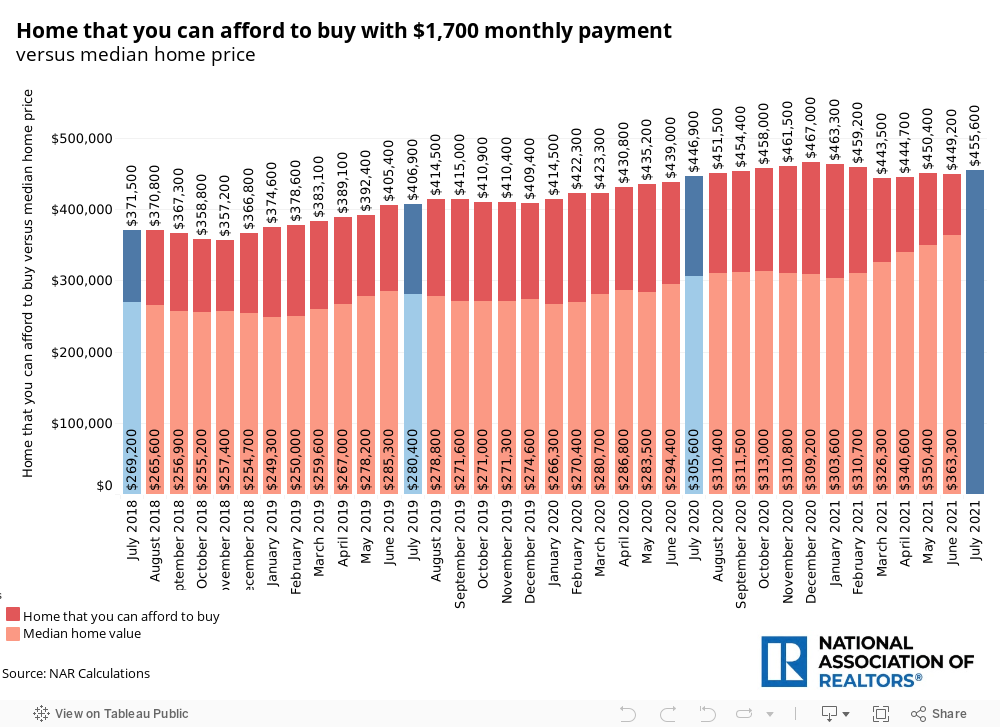

Since low mortgage rates increase homebuyers' purchase power, this also means that many prospective homebuyers may be able to afford to buy a more expensive home than they previously thought with the same budget. Let’s take a look at how much home you would be able to afford in the past three years.

Assuming you want to pay $1,700 per month for your home loan, you can currently buy a home with a value of $455,600. A year ago, when rates were higher at 3.02%, you were able to buy a home priced $446,900 with the same payment. Respectively, two years ago, while rates were over 3.7% you could buy a less expensive home ($406,900) and, three years ago, you could purchase an even less expensive home, about $370,000, as mortgage rates were 4.53%. Thus, in the last three years, the mortgage rate dropped by 1.66%, giving you the opportunity to buy a home which is $84,000 more expensive. Meanwhile, the value of the typical home has increased more than $94,000 in the last three years due to limited housing supply. Thus, when we compare with the median home prices, we are seeing that current homebuyers who pay $1,700 for their home loan can afford to buy a home which is 24% more expensive than the typical home compared to 38% three years earlier. Therefore, rising home prices diminish purchase power of prospective buyers although mortgage rates are near record lows.