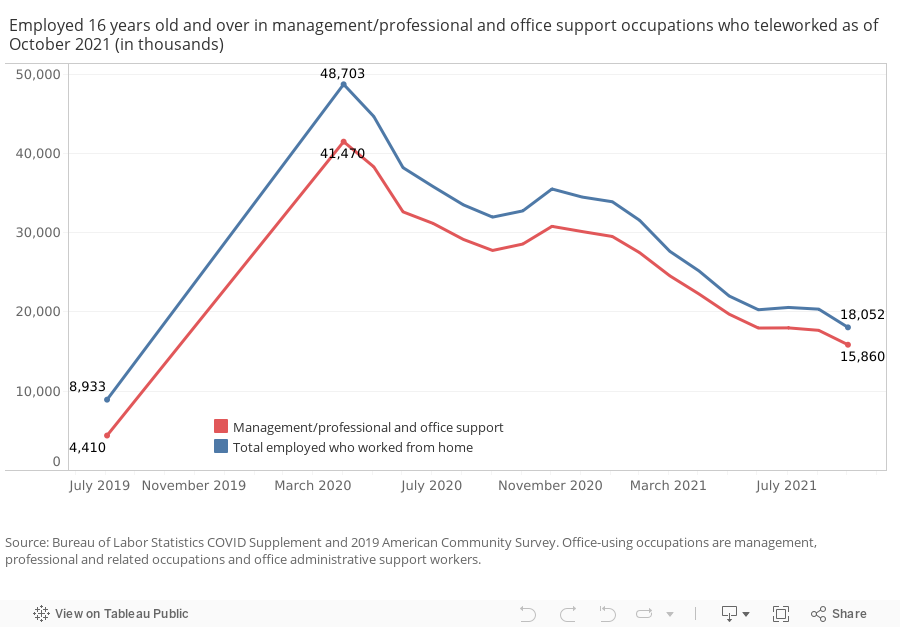

The demand for office space continues to remain in negative territory on the aggregate, as high to substantial transmission1 of the coronavirus delta variant continues to sustain a work-from-home approach, increasing the likelihood that a hybrid workstyle will become the dominant option in the future.

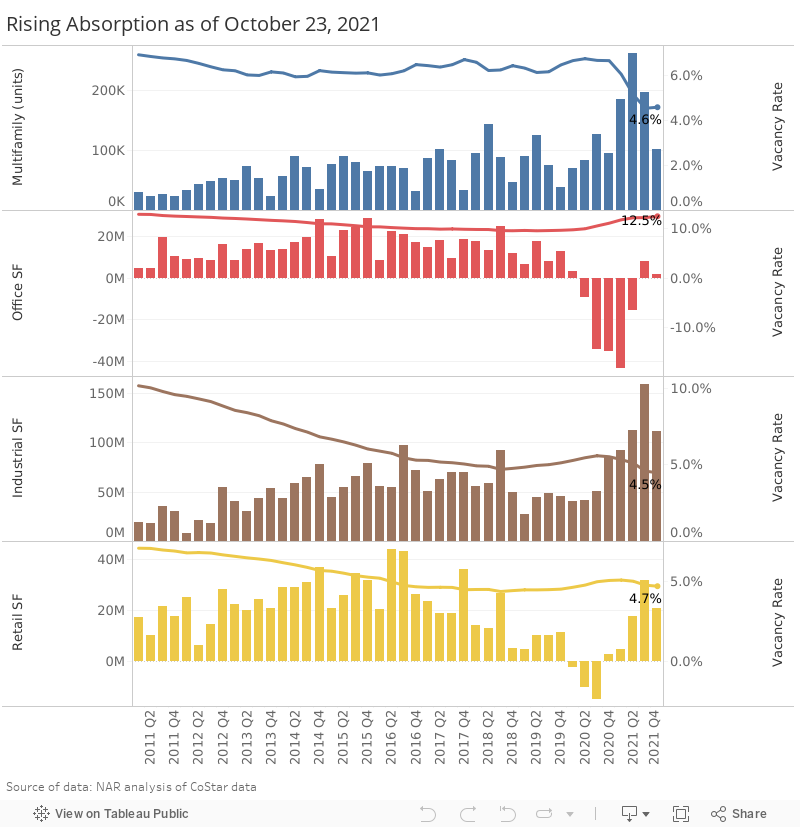

Since 2020 Q2 through September 19, 144 million square feet of office space has been released back to the market (negative net absorption), according to CoStar® market data. The office vacancy rate has increased to 12.4% (9.8% in 2020 Q1) and the average asking rent has declined year-over-year, at -0.4%. However, the headline figures mask the resiliency and recovery in secondary markets which are more numerous but which account for a lesser share of the office square footage that primary/gateway markets account for.

Gateway cities still struggling to recover lost office space, but secondary markets are thriving

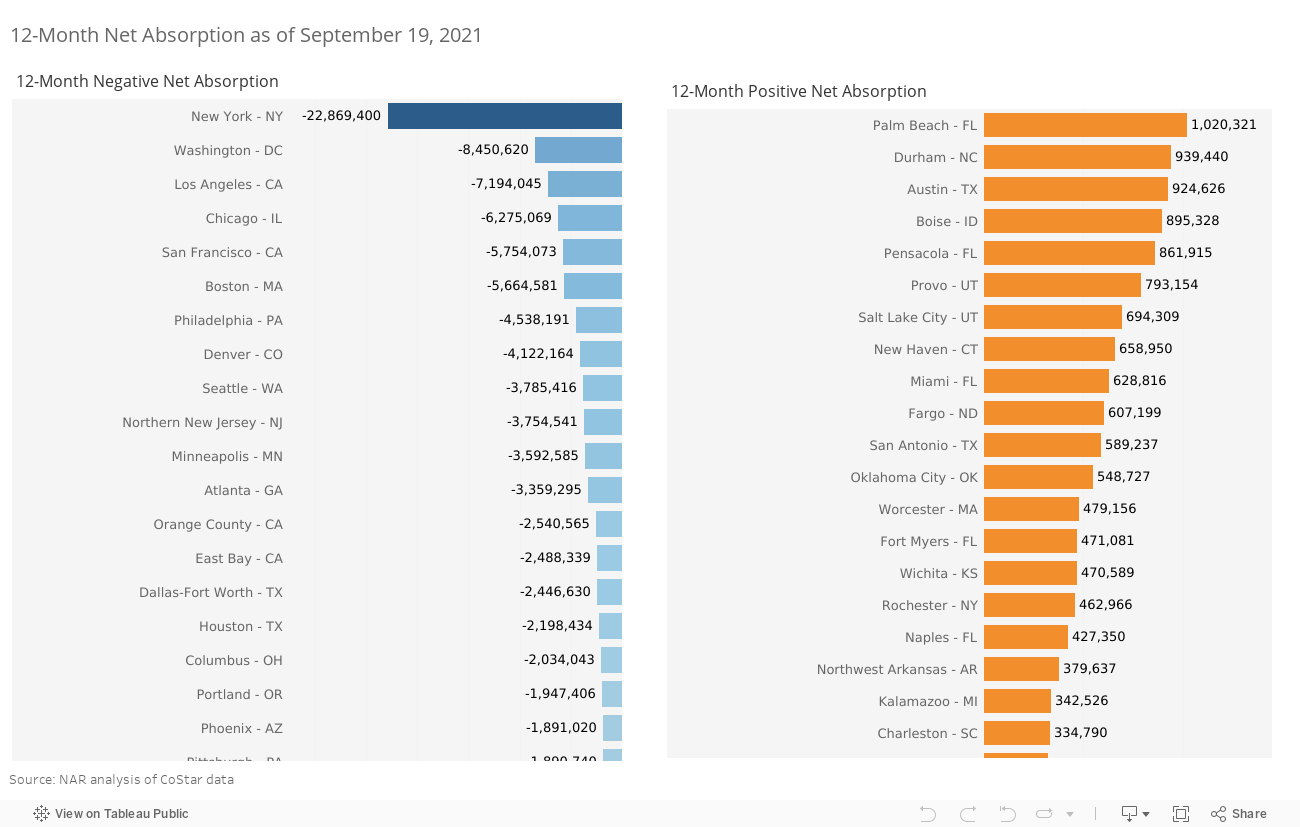

As of September 10, New York, Washington D.C., Los Angeles, Chicago, San Francisco, Boston, Philadelphia, Denver, Seattle, and Northern New Jersey have suffered the largest declines in occupancy over a 12-month period. Twenty-six of 390 markets have lost over 1 million square feet in office occupancy on a net basis over the past 12 months ending September 19.

However, secondary markets are experiencing rising occupancy, with the largest increases in Palm Beach, Durham, Austin, Boise, Pensacola, Provo, Salt Lake City, New Haven, Miami, Fargo, San Antonio, and Oklahoma, each of which absorbed at least 500,000 square feet of office space.

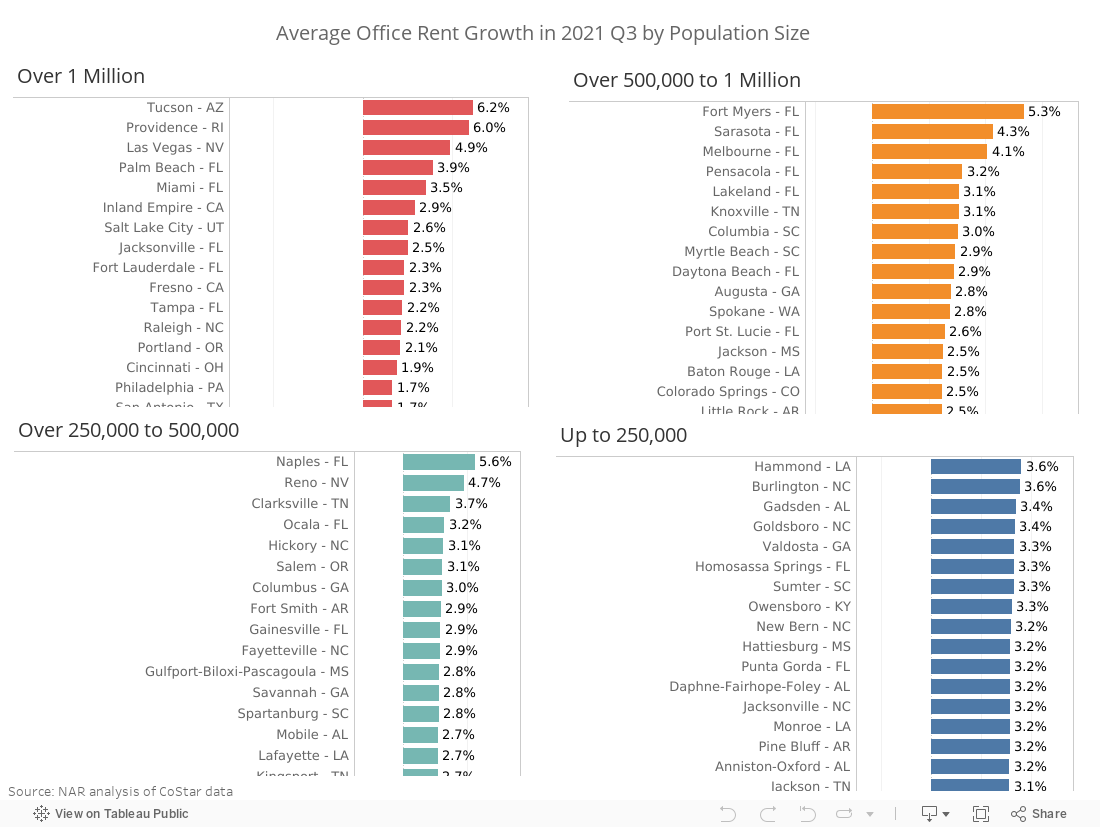

Florida is emerging as the “it” state when it comes to the office market, with several markets having positive net absorption: Palm Beach, Pensacola, Miami, Fort Myers, Naples, Port St. Lucie, Sarasota, Daytona Beach, Orlando, Lakeland, Tampa, Melbourne, Punta Gorda, and Sebring.

Asking rents still down nationally, but rising in many smaller markets

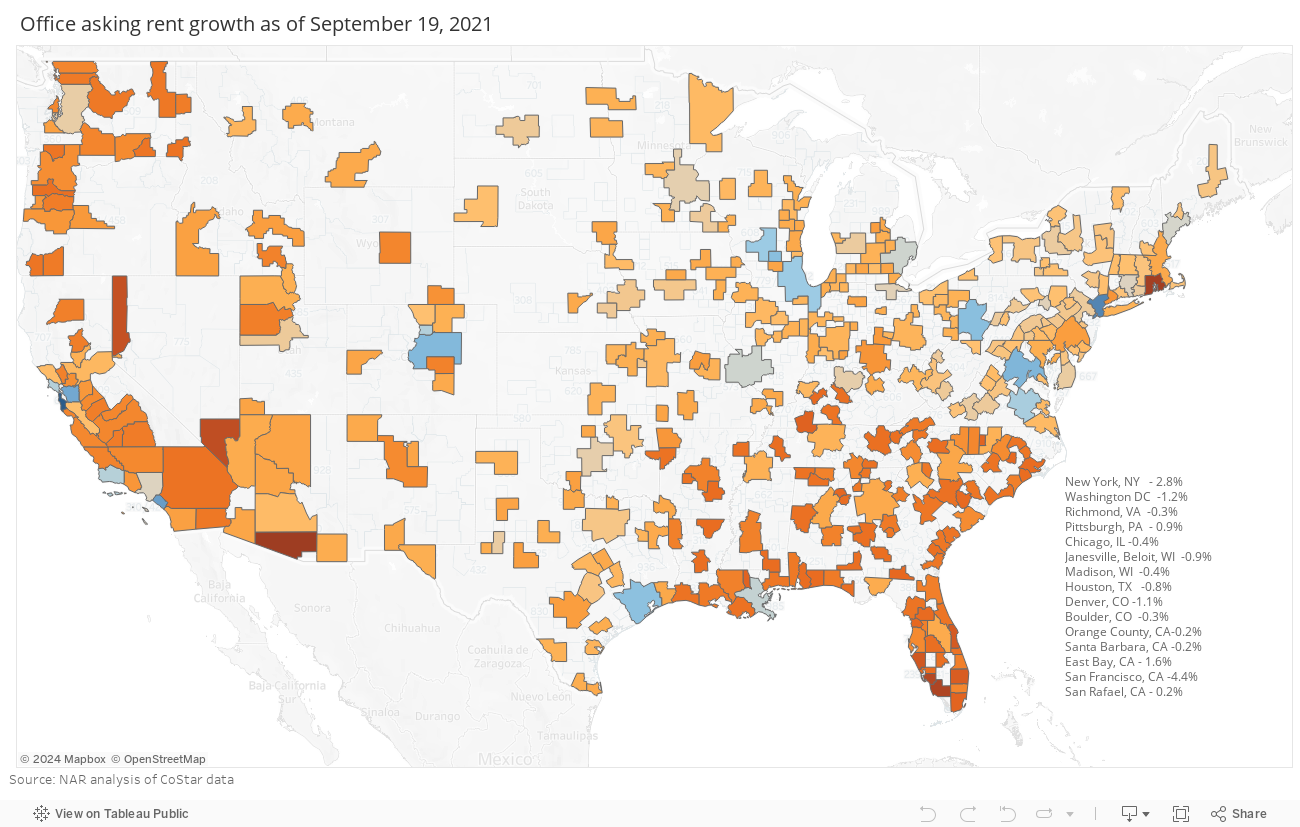

With falling occupancy and rising office vacancy rates, asking rents remained below the level recorded one year ago, down by 0.4% as of September 19, 2021. The national average rent growth is being pulled down by the rent declines in the large markets of San Francisco (-4.4%), New York (-2.8%), Orange County (-2%), East Bay (-1.6%), Washington, D.C. (-1.2%) and Denver (-1.1%).

However, office rents are up on a year-over-year basis in 365 out of 380 metro areas tracked by CoStar®. Secondary/tertiary metro areas are experiencing high rent growth, led by Tucson, Arizona (6.2%), Providence, Rhode Island (6%), Naples, Florida (5.6%), and Fort Myers, Florida (5.3%), and Las Vegas (4.9%).

Outlook: Office vacancy rates to remain above 10% in 2022

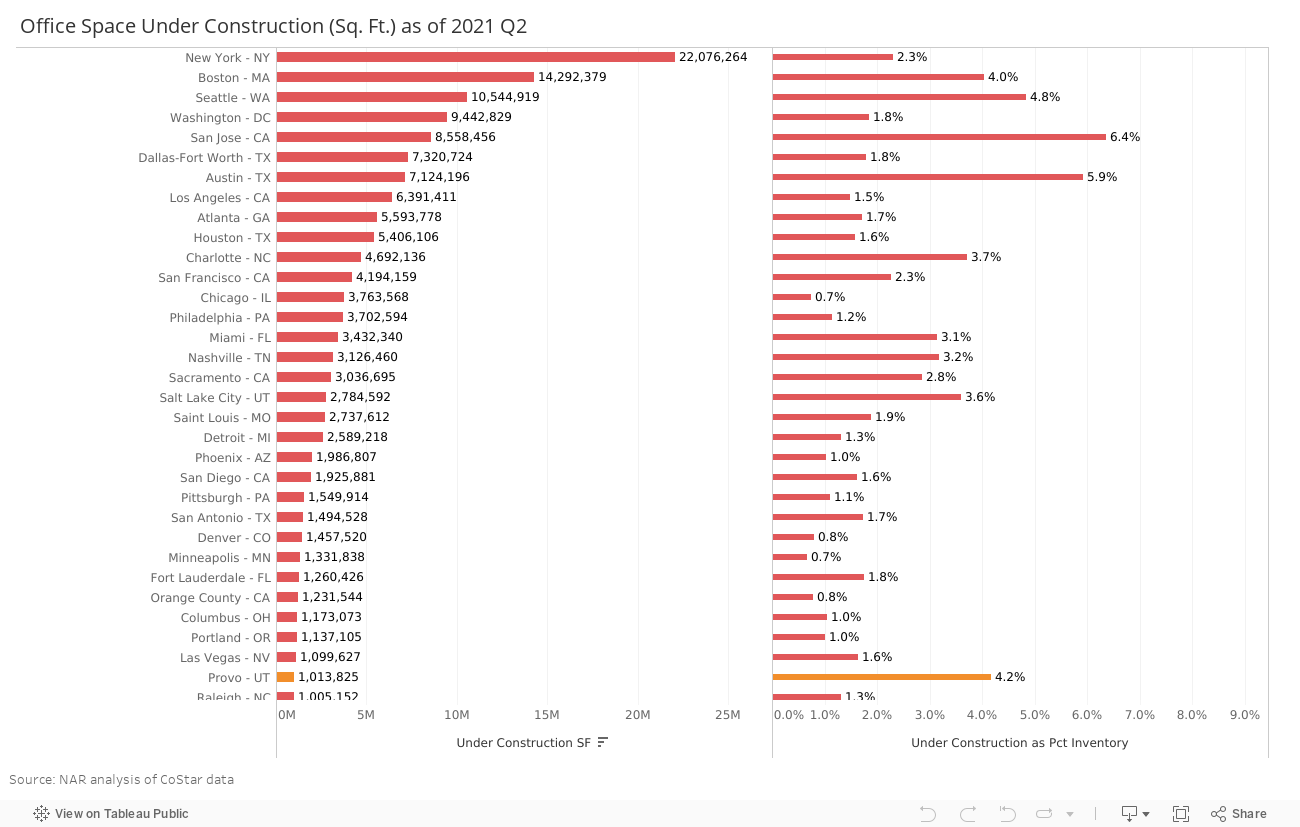

As of the second quarter of 2021, 144.3 million square feet of office space is under construction, equivalent to about 2% of the existing office space. If the space being constructed is mostly speculative, it will add to the already-elevated vacant inventory and will continue to depress rents in the primary markets until the office space is absorbed.

The largest construction projects are still happening in metro areas that are currently still suffering from declining occupancy: New York, Boston, Seattle, Washington D.C., San Jose, Dallas, Austin, and Los Angeles. In San Jose and Austin, the incoming supply amounts to about 6% of office space.

With the huge losses in office occupancy in these markets and the ongoing construction, office vacancy rates will likely remain above 10% in the next two years.

1 CDC reported as high to substantial transmission rates in 97% of counties as of the week of September 19, but that has gone down to 76% as of September 24. See https://covid.cdc.gov/covid-data-tracker/#county-view