Apartment occupancy has increased in nearly all markets since the pandemic

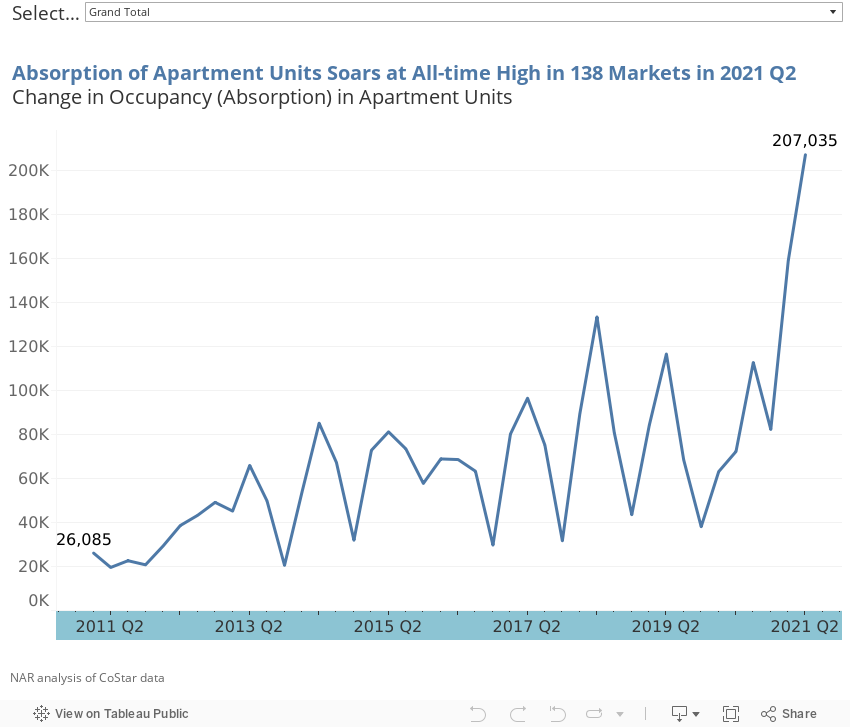

The apartment market is booming. Based on NAR's analysis of CoStar market data in 138 markets1, net absorption (change in number of occupied units) rose by 207,035 units in 2021 Q2 from the prior quarter. In 2019 Q2, a pre-pandemic period, net absorption was only 116,526 units, about half the current pace of absorption. During 2020 Q2 through 2021 Q2, 137 out of 138 areas experienced an increase in the number of occupied units (positive net absorption), with San Francisco as the only metro area that still had a negative net absorption of 2,730 units, according to NAR's analysis of CoStar data.

Decline in apartment occupancy due to pandemic was concentrated in very few markets

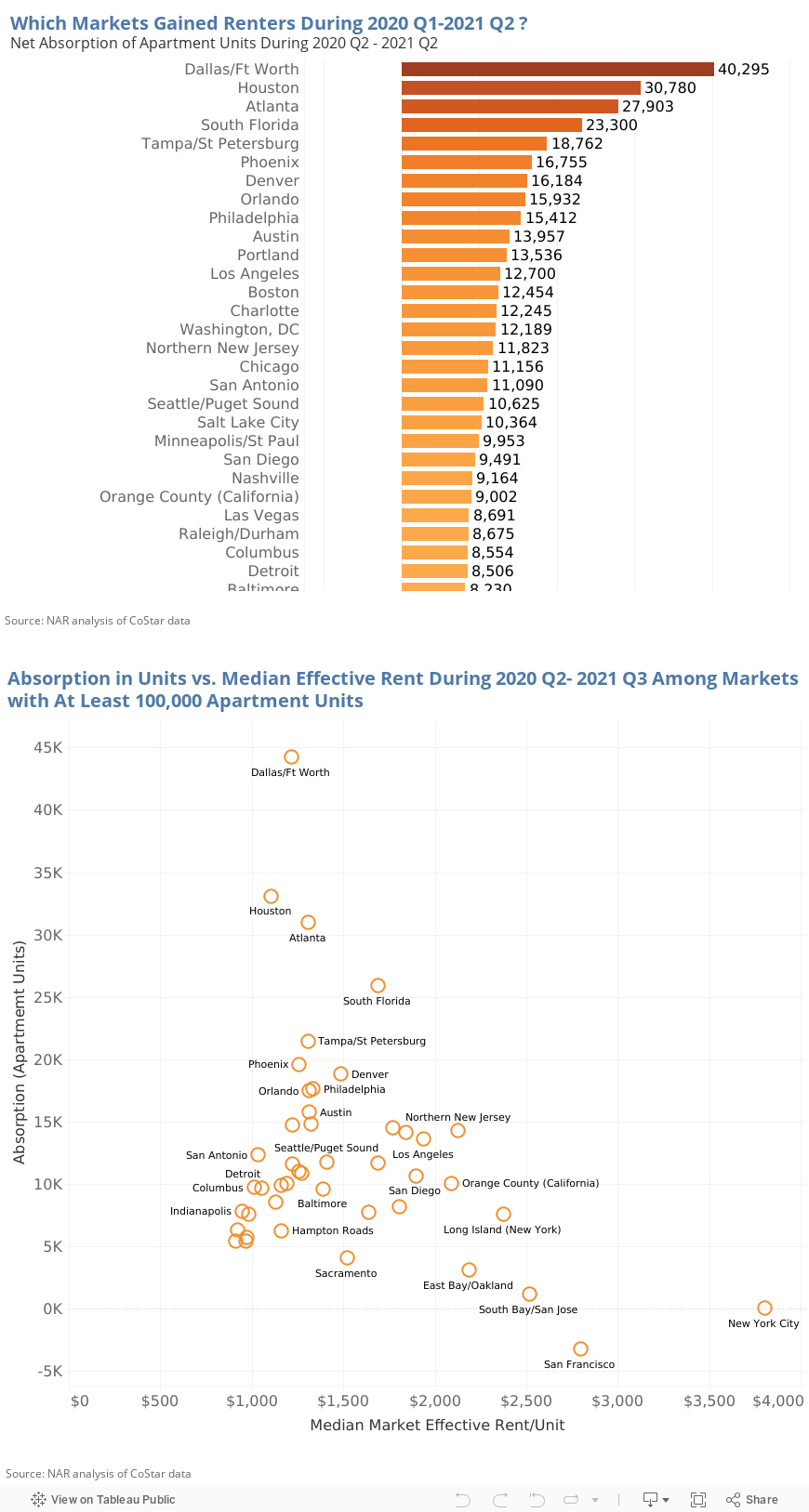

It is worth pointing out that the decline in apartment occupancy was concentrated in the New York City area and in the West Coast markets: San Francisco (-6,958 apartment units); New York City (-4,371 units); South Bay/San Jose (-2,791 units); East Bay/Oakland (-445 units); Chicago (-337 units); Pittsburgh (-71 units),and Yakima (-30 units).

Other large markets did not experience negative net absorption during any of the quarters since the pandemic. The largest gains in occupancy during 2020 Q2 – 2021 Q2 were in Atlanta, Austin, Boise, Dallas, Denver, Houston, Orlando, Philadelphia, Phoenix, and Portland.

One reason for the decline in occupancy is the makeup of the workforce. West Coast markets have a heavy concentration of technology workers2, while New York City is a major financial center, headquarters to many corporations, and a tourist destination, so apartment rental demand plummeted at the height of the pandemic (2020 Q2) in New York City and the West Coast markets when workers started working from home and as business and personal leisure and travel were cut back. As of June 2021, on a national basis, 50% of mathematical and computer workers and 40% of legal occupation workers are still working from home.3 The impact of the pandemic was also brief, and by the 2020 Q4, occupancy had started to pick up in these markets.

In addition to the profile of workers in the markets that suffered huge declines in occupancy, another reason that can explain why occupancy did not decline (or declined little) in the other markets could be due to differences in rent and housing affordability, which heavily bears on job creation among companies who want to locate their businesses in a market area that is attractive to workers because housing is affordable. In New York City, the median effective rent during 2020 Q2- 2021 Q3 was $3,764; in San Francisco, $2,746; and in East Bay/Oakland, $2,163. These are high rents compared to the median effective rents in Dallas, at $1,201; in Houston, at $1,100; in Atlanta, at $1,284; or in Phoenix, at $1,231.

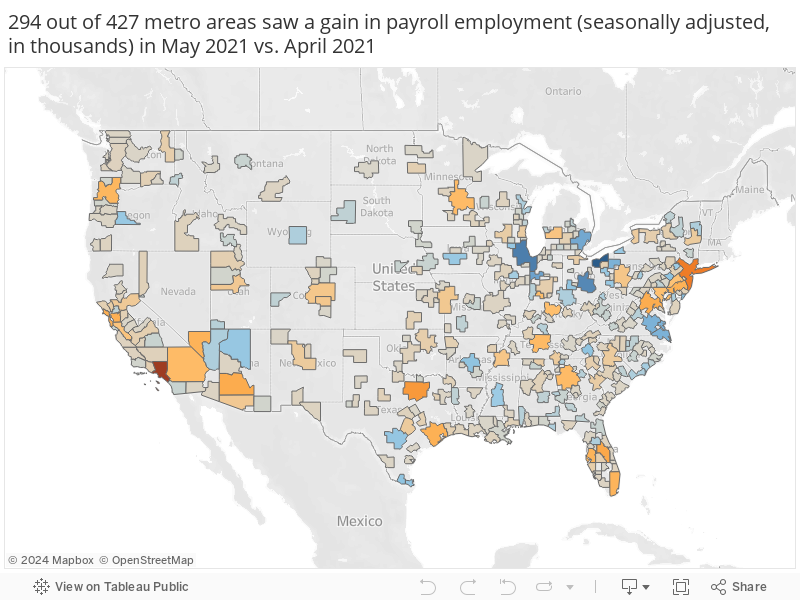

In May 2021, 294 out of 427 metro areas had an increase in nonfarm payroll employment (seasonally adjusted) compared to the prior month. Dallas-Fort Worth created 14,900 jobs; Houston, 8,800 jobs; Atlanta, 6,000 jobs; and Phoenix, 10,200 jobs.

Rent outlook

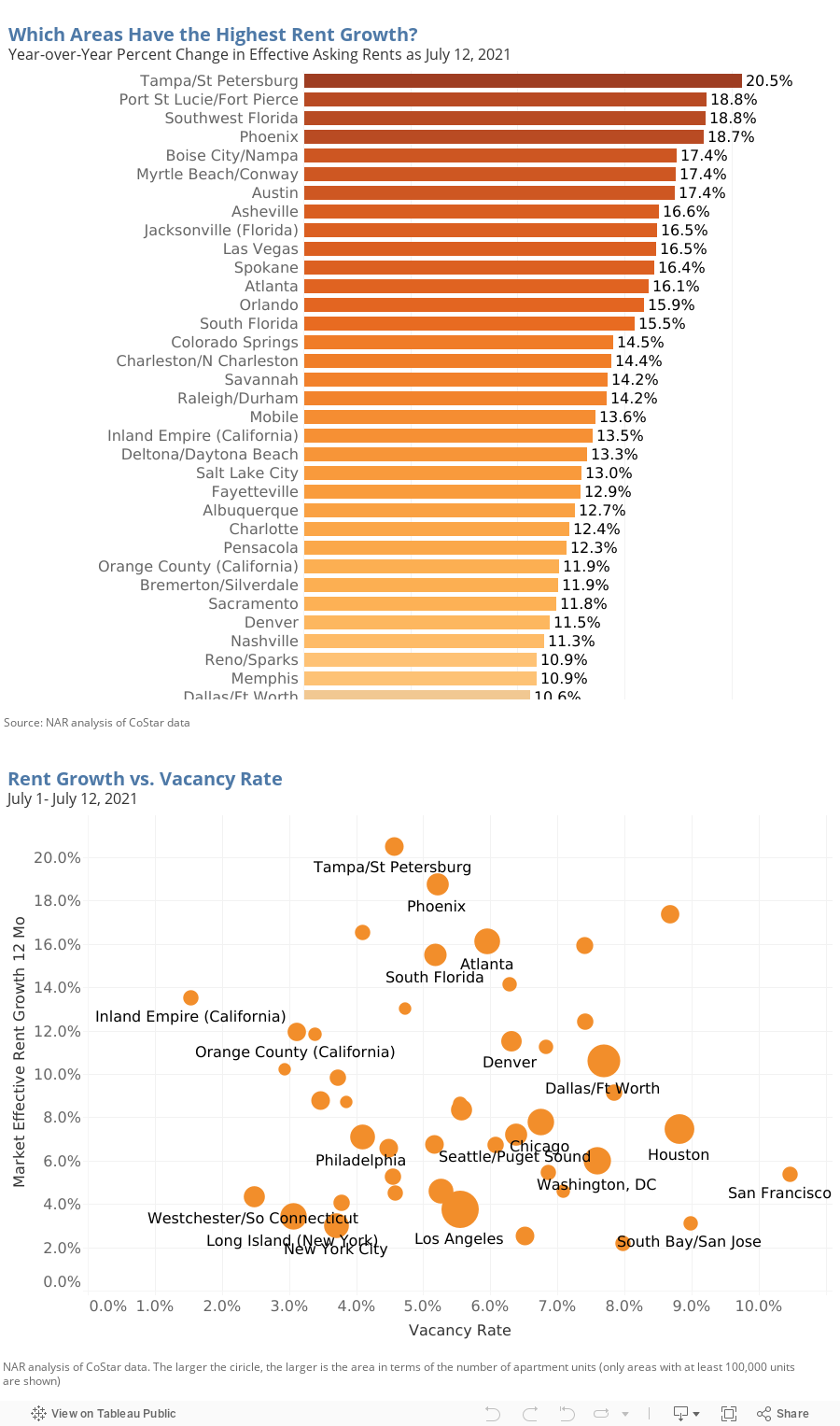

Due to strong demand for apartments, rents are rising strongly. Only South Bay/San Jose and San Francisco have lower rents as of 2021 Q2 compared to one year ago. In all markets, rents are up from one year ago. In New York City and Oakland, rents have recovered, with the effective rents up by less than 1% from one year ago.

In 39 markets, rents are rising at a double-digit pace. As of 2021 Q2, the steepest rent increases on a year-over-year basis were in Port St. Lucie/Fort Pierce (21%), Tampa/St. Petersburg (20%), Myrtle Beach (20%), Phoenix (19%), Boise (18%), Las Vegas (18%), Spokane (17%), Atlanta (16%), Jacksonville (16%), and Savannah (16%).

Expect markets with low vacancy rates to show strong rent growth, such as the California markets: Inland Empire, Orange County, San Diego, Los Angeles, and Sacramento.

Other markets with strong rent growth and low vacancy rates will likely continue to experience sustained rent growth—markets like Tampa, Phoenix, Las Vegas, South Florida, Philadelphia, and Hampton Roads (Virginia).

Vacancy rates are not as tight in Atlanta, Dallas, and Houston, but rents have been growing at a strong pace due to the net in-migration in these areas.

Rents are likely to rise a bit in Oakland, San Jose, and San Francisco as more workers return to the office, but the high vacancy rates will keep rents growing at a modest pace compared to other markets.1 These 138 markets tracked by CoStar consisted of 16.6 million apartment units, or about 60% of the 27.6 million renter-occupied housing units as of 2019 based on the American Community Survey

2 14% of San Francisco's workforce is in professional, scientific and technical services industry compared to 7% nationally.

3 US Bureau of Labor Statistics COVID-19 CPS supplemental data