The Paycheck Protection Program (PPP) is a program funded under the $2.2 trillion CARES Act to provide a direct incentive for small businesses to keep their workers on the payroll. The $349 billion PPP program (Round 1) opened on April 3, but it was nearly exhausted as of April 16. The PPP program reopened on April 27 after a $310 billion supplemental funding (Round 2) was approved by Congress. The PPP incentives businesses to keep workers on their payroll by forgiving the loan if all employees are kept on the payroll for eight weeks and the money is used for payroll, rent, mortgage interest, or utilities. However, at least 75% of the forgiven amount must have been used for payroll. It is open to any small business concern that meets SBA’s size standards (either the industry based sized standard or the alternative size standard) and to sole proprietors, independent contractors, and self-employed persons. The loan amount is equivalent to 2.5 months the average monthly payroll costs (includes net profits for self-employed)1.

The Small Business Administration has released data that as of May 8, there were 4.2 million loans granted PPP funding totaling $531.2 billion. The PPP loan application form2 asks the applicant for the number of employees, but employment associated with the loans is not reported by the Small Business Administration.

So how many paid and self-employed workers are potentially being saved from joining the ranks of the unemployed with this program? Using employment by size of firm data from the 2017 Statistics of US Business (latest available) and the number of self-employed 16 years old and over from the 2018 American Community Survey (latest available), I estimate that as of May 8, the PPP program is potentially saving 15 million jobs or 20% of the 143.8 million workers who are paid by firms or who are self-employed workers. The 4.2 million loans account for 20% of 21.2 million firms with less than 500 workers and self-employed workers.

Methodology

The Small Business Administration reports the number of loans for Round 1 and Round 2 at the state level. The Statistics of US Business also has information on the employment size of firms. I assumed that firms with less than 500 employees will qualify for the PPP loan, although other industries can also qualify for a PPP loan based on SBA annual receipts or size standards. For example, the SBA standard for what constitutes a small business is based on annual receipts, not size standards.

The Statistics of US Business excludes data on self-employed individuals, employees of private households, railroad employees, agricultural production employees, and most government employees. Businesses operating without an Employer Identification Number (EIN) and businesses with an EIN but without employees, are excluded from the SUSB universe.

Because the Statistics of US Business excludes self-employed, I added the self-employed individuals 16 years old and over from the American Community Survey to get the total number of firms with employment less than 500 employees and self-employed individuals. I assumed that one self-employed individual counts as one “firm”.

I then got the ratio of the number of PPP loans approved for each state to the sum of the number of firms with less than 500 employees and the number of self-employed workers. Nationally, the ratio is 20%, but it varies in each state.

I used this state-level ratio and multiplied it to the number of employees in firms with less than 500 workers in each state and to the number of self-employed in each state. Nationally, I got 15 million workers who are in firms with less than 500 employees and who are self-employed.

State-level results

We can have an estimate of the share of PPP loans to the number of firms with less than 500 employees and self-employed at the state-level. Nationally, the 4.2 million PPP loans as of May 8, 2020, represent 20% of the nearly 21 million firms with less than 500 employees (5.98 million, 2017 SUSB) and 15 million self-employed (2018 ACS). By state, North Dakota had the highest share, at 29%. The lowest shares are in California and Arizona, each at 16%. In Washington, the PPP loans represent 17% of the firms with less than 500 employees and self-employed. In New York, the share is 20%, and Illinois, the share is 22%.

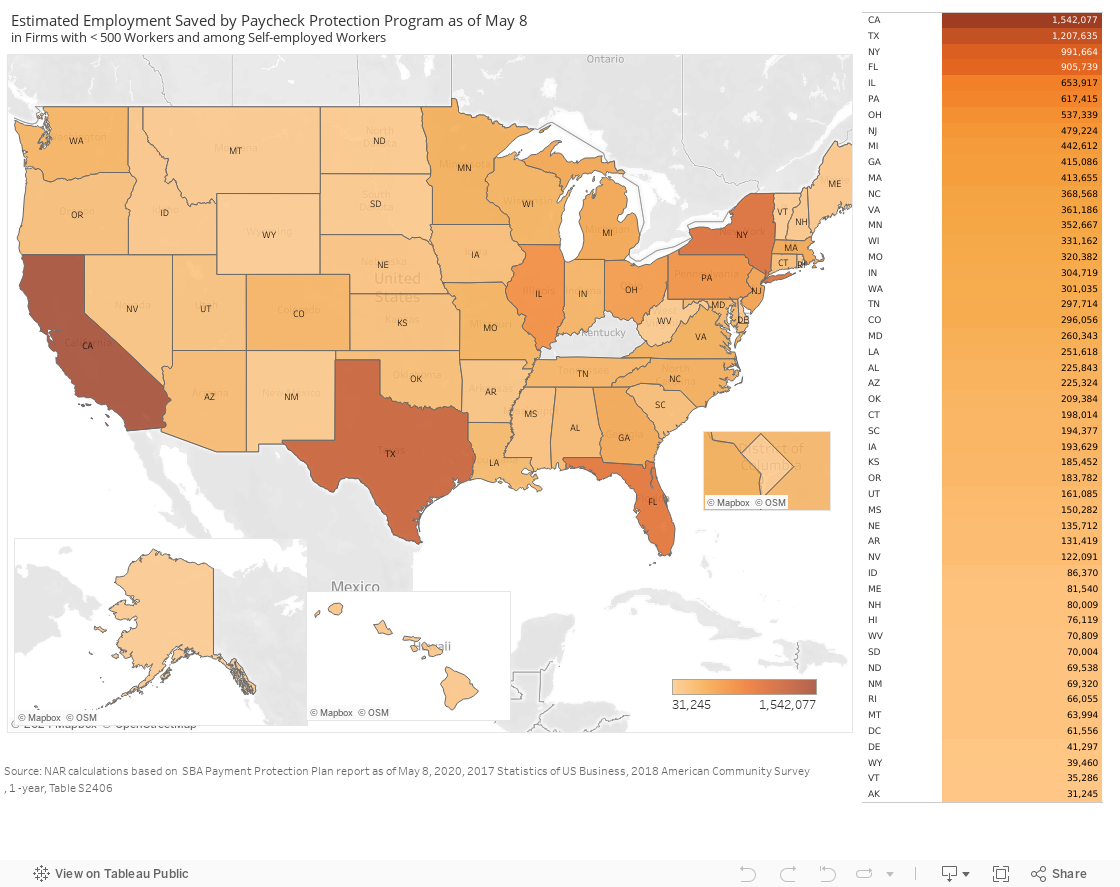

Nationally, the PPP loans are associated with 14.8 million paid workers, of which 11.8 million are paid employees and nearly 3 million are self-employed. The states with the highest number of paid workers and self-employed expected to have been saved by the PPP loans are California (1.54 million), Texas (1.2 million), New York (991,664), and Florida (905,739), and Illinois (653,917).

To note, the 15 million could be underestimated because the SUSB data is as of 2017, and there are now more establishments than in 2017, indicated by the 2 million jobs generated per year on average in 2018 and 2019.

1 See guidelines on calculating the loan amount https://www.sba.gov/sites/default/files/2020-04/How-to-Calculate-Loan-Amounts.pdf

2 https://www.sba.gov/sites/default/files/2020-04/PPP%20Borrower%20Application%20Form.pdf